The Psychology of Money: Why Smart People Stay Poor and How Behavior Shapes Wealth

By : maryam

Most people will never become wealthy—not because they don’t work hard enough, but because they keep making financial decisions with emotions they don’t even understand. They study money, chase advice, follow strategies… yet still end up stuck in the same financial cycle for years.

The uncomfortable truth is that being “smart” has almost nothing to do with building wealth. Some of the most educated and intelligent people are living paycheck to paycheck, while others with average knowledge quietly grow their wealth in the background without anyone noticing.

The real difference is not what people know about money, but what money does to their mind. Fear makes them sell too early. Greed makes them take unnecessary risks. Comparison pushes them to spend more than they earn. And impatience destroys years of potential growth in a single decision.

Wealth is not a math problem. It is a behavior problem—and most people never realize they are the problem.

+Introduction + Money is emotional before mathematics + Stories about money

+Appearance vs real wealth + chasing more + fear and action

+Luck vs habits + consistency + invisible power of small actions

+Intelligence vs wealth + childhood influence + comparison

+Lifestyle inflation + enough concept + small decisions

+Spending psychology + patience + repeated mistakes + freedom

+Financial confidence + easy money + opportunity cost + daily choices

+FAQ + conclusion + about the author

Why Intelligence Alone Will Never Make You Wealthy

For decades, people have been taught that financial success is primarily the result of intelligence, education, or professional expertise. Society often assumes that individuals with advanced degrees, exceptional analytical skills, or high-paying careers are naturally better at managing money. While these qualities can certainly help people generate income, they do not automatically lead to wealth. In reality, history provides countless examples of highly educated professionals—including doctors, lawyers, engineers, and even financial experts—who have struggled with debt, poor spending habits, or financial insecurity. At the same time, there are individuals with average educational backgrounds who quietly accumulate significant wealth through consistent financial behavior. The difference between these two groups rarely lies in intelligence alone; instead, it lies in how they think about money, how they respond to emotions, and how they make decisions when faced with uncertainty.

One of the biggest misconceptions about wealth is that it is created by a few extraordinary financial decisions. In reality, wealth is usually the result of hundreds of ordinary decisions repeated consistently over many years. Every choice to save a portion of income instead of spending it immediately, every decision to avoid unnecessary debt, every investment made with patience rather than excitement, and every financial goal pursued despite short-term distractions contributes to long-term financial security. These decisions may seem insignificant on any given day, but their cumulative effect becomes enormous over time. This is why financial success often appears mysterious to outsiders. They notice the final outcome but rarely see the thousands of small behaviors that produced it.

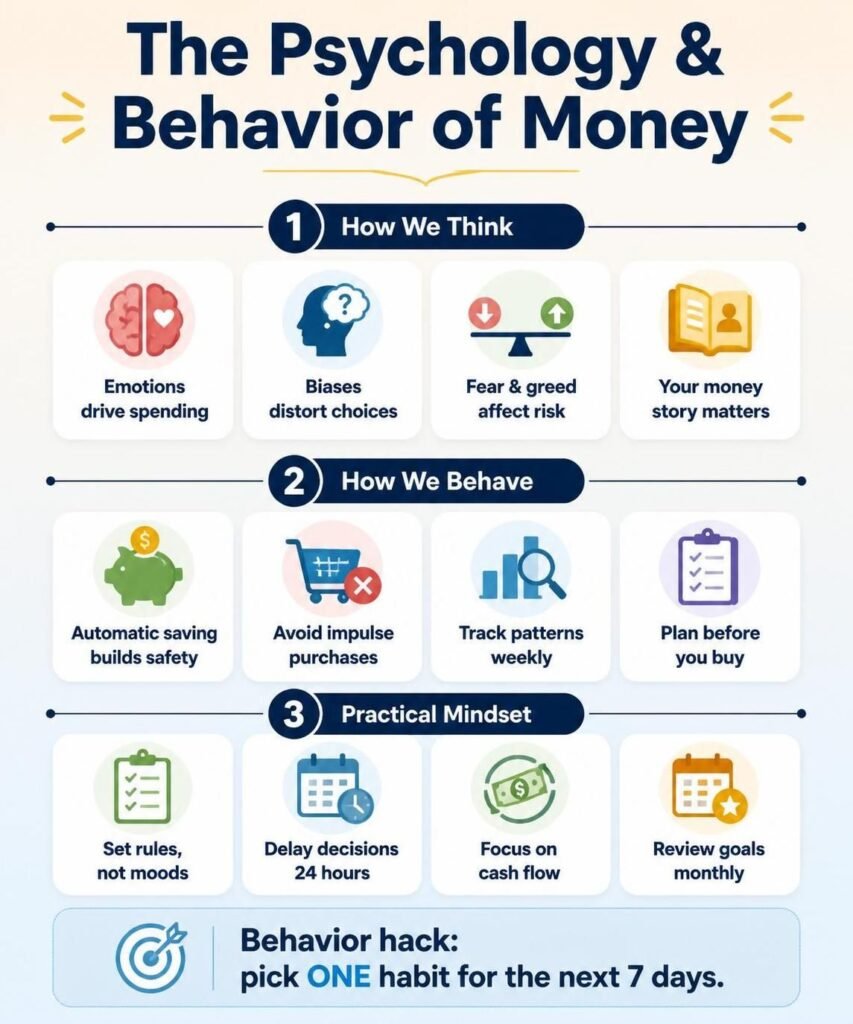

Behavioral economists have spent decades studying why intelligent people frequently make irrational financial decisions. Their research demonstrates that the human brain was not designed to optimize long-term wealth. Instead, it evolved to prioritize immediate survival and instant rewards. Thousands of years ago, preferring immediate resources over uncertain future benefits increased the chances of survival. Today, however, the same psychological tendency encourages impulsive spending, excessive borrowing, emotional investing, and the constant pursuit of short-term satisfaction. Modern financial markets require patience, delayed gratification, and emotional stability—qualities that often conflict with our natural instincts. Understanding this conflict helps explain why knowledge alone rarely changes financial outcomes. Knowing what should be done is entirely different from consistently doing it.

Another reason intelligence does not guarantee financial success is that money is deeply connected to identity and emotions. Every financial decision carries psychological meaning beyond its numerical value. Purchasing an expensive car, for example, may have less to do with transportation than with social recognition or personal achievement. Likewise, refusing to invest may have less to do with market analysis than with a fear of uncertainty created by previous negative experiences. People often believe they are making rational financial decisions when, in reality, those decisions are driven by invisible emotional forces. Fear, pride, anxiety, comparison, and the desire for approval quietly influence financial behavior far more often than spreadsheets or investment reports.

Successful wealth builders recognize this psychological reality. Rather than assuming they are perfectly rational, they acknowledge that emotions will always influence their decisions. As a result, they design financial systems that reduce the impact of those emotions. They automate savings, create long-term investment plans, establish emergency funds before taking financial risks, and avoid making important decisions during periods of excitement or panic. Instead of relying on willpower alone, they create environments that encourage disciplined behavior. This approach reflects an important principle: sustainable wealth is rarely built by making brilliant decisions under pressure; it is built by creating habits that continue working even when motivation disappears.

Ultimately, financial success depends less on the size of a person’s income than on the consistency of their behavior. A high income without discipline often leads to lifestyle inflation, where every increase in earnings is matched by an increase in spending. Conversely, a moderate income combined with thoughtful financial habits can gradually produce remarkable levels of financial independence. Intelligence may open opportunities to earn more, but behavior determines whether those opportunities become lasting wealth. Understanding this distinction shifts the focus away from searching for perfect investment strategies and toward developing the psychological habits that support sound financial decisions throughout life.

The Hidden Influence of Childhood on Financial Decisions

Most people believe that their financial habits begin when they receive their first paycheck. In reality, those habits often begin much earlier. Long before we earn, save, or invest money, we develop beliefs about it by watching the people around us. Children absorb financial attitudes from parents, relatives, teachers, and even the communities in which they grow up. They notice whether money is discussed calmly or with anxiety, whether spending is carefully planned or impulsive, and whether wealth is viewed as an opportunity or as something to distrust. These early observations quietly become the foundation of adult financial behavior.

A child who grows up in a household where money is always associated with stress may enter adulthood believing that financial security is impossible, regardless of how much they eventually earn. Even after receiving promotions or building a successful career, they may continue to feel anxious about every expense because their emotional relationship with money was shaped long before they understood budgeting or investing. On the other hand, someone raised in an environment where spending was used to celebrate every achievement may develop the habit of rewarding themselves with purchases whenever they experience success, regardless of whether those purchases fit their financial goals.

These childhood experiences often become invisible financial rules. Some people unconsciously believe that saving money means sacrificing happiness. Others believe that carrying debt is simply a normal part of adult life because it was common in their family. Some grow up thinking wealthy people are greedy, while others see wealth as a symbol of freedom and responsibility. These beliefs are rarely questioned because they feel natural, even though they were inherited rather than consciously chosen.

The encouraging news is that financial beliefs are not permanent. Once people recognize where their attitudes come from, they can begin replacing automatic reactions with intentional decisions. Understanding your financial past does not change what happened during childhood, but it gives you the opportunity to prevent old experiences from controlling your future. The first step toward changing financial behavior is often recognizing that many of your money habits were learned, not inherited by nature.

Why Comparison Is One of the Fastest Ways to Destroy Wealth

One of the greatest psychological challenges in modern life is the constant temptation to compare ourselves with others. Social media has made this habit stronger than ever before. Every day, people are exposed to carefully selected images of luxury vacations, expensive cars, designer clothing, and beautiful homes. What they rarely see are the financial sacrifices, loans, or personal struggles hidden behind those images. As a result, many individuals begin measuring their financial success against incomplete and often unrealistic pictures of other people’s lives.

Comparison changes the way people spend money. Instead of asking whether a purchase improves their own quality of life, they begin asking whether it will impress others. This subtle shift can have enormous financial consequences. A perfectly reliable car suddenly feels inadequate because someone else owns a newer model. A comfortable home no longer seems enough after seeing larger houses online. The desire to keep up with others gradually replaces the goal of building long-term financial security.

This behavior creates a cycle that is difficult to escape. As incomes increase, spending often increases at the same pace because people continue comparing themselves with individuals who earn even more. No matter how much they achieve, there is always someone with a larger salary, a bigger business, or a more luxurious lifestyle. Chasing that endless competition consumes resources that could have been invested, saved, or used to create greater financial freedom.

People who achieve lasting wealth usually adopt a different perspective. Instead of competing with the lifestyles of strangers, they focus on their own financial objectives. They understand that money is a personal tool, not a public performance. Their decisions are guided by future goals rather than temporary approval. Ironically, the less they feel the need to prove their success to others, the stronger their financial position often becomes. Real wealth grows quietly, while the need to appear wealthy can become surprisingly expensive.

The Dangerous Comfort of Lifestyle Inflation

Receiving a salary increase is one of the most satisfying moments in a professional career. After years of hard work, better pay feels like a well-deserved reward. However, many people unknowingly turn this positive event into a long-term financial problem through a phenomenon known as lifestyle inflation. Instead of allowing additional income to strengthen their financial future, they immediately increase their spending to match their new earnings.

Lifestyle inflation rarely happens all at once. It usually begins with small upgrades that seem harmless. A slightly more expensive apartment, frequent restaurant visits, premium subscriptions, luxury clothing, or a newer vehicle may each appear reasonable on their own. Over time, however, these higher expenses become permanent parts of everyday life. Eventually, the individual who once lived comfortably on a modest salary discovers that even a much larger income no longer feels sufficient.

The greatest danger of lifestyle inflation is that it creates the illusion of progress without improving financial security. Someone earning twice as much as they did five years ago may still experience the same level of financial stress because every increase in income has been matched by an increase in expenses. Their standard of living improves, but their financial resilience remains unchanged.

People who build sustainable wealth often respond differently to higher earnings. Rather than viewing every raise as permission to spend more, they treat it as an opportunity to increase savings, expand investments, or strengthen their emergency fund. They still enjoy the rewards of their success, but they avoid allowing temporary excitement to create permanent financial obligations. This balanced approach enables income growth to translate into genuine wealth instead of simply financing a more expensive lifestyle.

The Psychology of “Enough”

One of the biggest reasons people never feel financially satisfied is that they never define what “enough” actually means. Instead of setting a personal standard for success, they allow society to define it for them. As their income grows, so do their expectations. A salary that once seemed life-changing eventually feels ordinary, not because it has lost its value, but because the mind quickly adapts to improved circumstances. This psychological process, often called hedonic adaptation, explains why material achievements provide only temporary satisfaction before becoming the new normal.

The danger of this mindset is that it creates an endless cycle. Every financial milestone is replaced by another goal before there is time to appreciate it. A larger home leads to the desire for a better neighborhood. A newer car leads to wanting a luxury model. A successful business creates pressure to build an even bigger one. Ambition itself is not the problem; the problem is pursuing growth without ever asking whether that growth actually improves your life.

People who achieve lasting financial peace usually have a clear definition of enough. They know the lifestyle they want, the level of security they need, and the experiences they value most. Because of this clarity, they are less likely to waste money trying to impress others. Their financial decisions are guided by purpose rather than comparison. Knowing when enough is truly enough does not limit success—it prevents success from becoming an endless race that can never be won.

Why Small Decisions Matter More Than Big Ones

Many people believe that wealth is created through one extraordinary decision: investing in the perfect company, launching a successful business, or receiving a large inheritance. Although these events can accelerate financial growth, they are not what sustains it. Most fortunes are built through small, consistent decisions that seem almost insignificant in the moment.

Choosing to save a percentage of every paycheck may not feel exciting, but repeating that habit for twenty years can produce remarkable results. Preparing meals at home several times a week, avoiding unnecessary subscriptions, or investing regularly regardless of market conditions may appear ordinary. Yet these routine behaviors often have a greater long-term impact than a single brilliant investment.

Small financial mistakes work the same way. Buying something unnecessary once is rarely a serious problem. However, making impulsive purchases every week gradually becomes a habit that quietly drains thousands of dollars over the years. Because these expenses are spread across time, people rarely notice their true cost.

Financial success is rarely the result of one life-changing moment. More often, it is the outcome of hundreds of ordinary choices that either move you closer to your goals or further away from them. The challenge is that these choices rarely feel important when they happen. Their real power becomes visible only after years of consistency.

The Difference Between Spending for Happiness and Spending for Approval

Money has the ability to improve life, but only when it is spent intentionally. Many purchases are driven by genuine needs or experiences that create lasting satisfaction. Others are motivated by something entirely different: the desire to gain recognition, admiration, or social acceptance. While these motivations may seem similar, they often produce very different outcomes.

When people spend money to improve their own lives, they usually make thoughtful decisions. They invest in education, health, meaningful travel, comfortable living spaces, or experiences shared with family and friends. These purchases often continue providing value long after the money has been spent because they strengthen well-being or create lasting memories.

Spending for approval follows a different pattern. The goal is not personal satisfaction but external validation. Expensive clothing, luxury accessories, or the latest technology may provide a temporary sense of confidence because they attract attention from others. However, that feeling fades quickly, encouraging another purchase in search of the same emotional reward. This creates a cycle in which satisfaction depends on constant spending.

Understanding the difference between these two motivations can dramatically improve financial decisions. Before making a major purchase, it is worth asking a simple question: Would I still want this if nobody else ever saw it? The answer often reveals whether the decision is based on personal value or social pressure. People who consistently choose the first path usually find that their money creates more happiness while requiring far less of it.

Why Patience Is One of the Most Valuable Financial Skills

Modern life encourages speed. We expect instant deliveries, immediate replies, and quick results in almost every area of life. Unfortunately, this mindset often carries over into personal finance, where many people expect wealth to grow just as quickly. When investments fail to produce impressive returns within a few months, they become impatient. When a business takes years to become profitable, they assume it has failed. In reality, wealth rarely grows in a straight line, and it almost never grows overnight.

One of the most powerful forces in finance is time. A modest investment that remains untouched for decades can outperform a much larger investment that is constantly bought and sold. This happens because returns have the opportunity to build on previous returns, creating a compounding effect that becomes stronger with each passing year. At first, the progress appears slow, which is why many people quit before they experience the most rewarding stage of growth.

Patience also protects people from emotional mistakes. Investors who constantly react to market news often buy when prices are high because they fear missing out, then sell when prices fall because they fear losing more money. These decisions are driven by emotion rather than logic, and they often produce disappointing results. Patient investors understand that temporary market movements are a normal part of long-term investing. Instead of trying to predict every change, they focus on remaining consistent with a well-designed plan.

Developing patience does not mean ignoring opportunities or refusing to adapt. It means understanding that meaningful financial progress requires time. The ability to stay committed to good decisions, even when results are not immediately visible, is one of the qualities that separates successful wealth builders from those who constantly start over.

Why People Repeat the Same Financial Mistakes

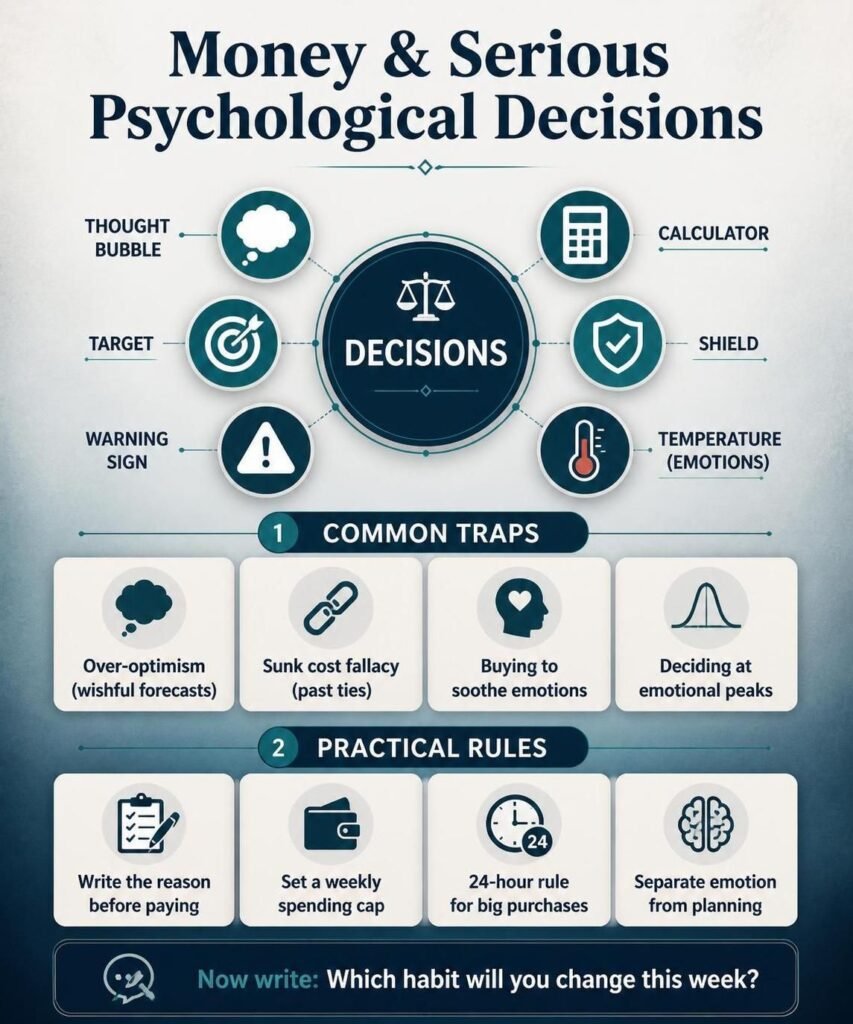

One of the most interesting aspects of human behavior is that people often repeat financial mistakes even after experiencing their negative consequences. Someone may accumulate credit card debt, spend years paying it off, and then gradually return to the same spending habits. Others lose money by making emotional investment decisions but continue reacting to market fear every time prices decline. Knowledge alone is often not enough to change behavior because habits are deeply connected to emotions and routines.

The brain naturally seeks familiar patterns, even when those patterns are harmful. Financial habits become automatic through repetition, which means they require very little conscious effort. This is why changing them can feel surprisingly difficult. A person who has spent years using shopping as a way to reduce stress may continue doing so even after realizing the financial damage it causes. The behavior is no longer just about money—it has become an emotional response.

Creating better financial habits requires replacing old routines rather than simply trying to eliminate them. Instead of making impulsive purchases after a stressful day, someone might choose to exercise, read, or spend time with family. Likewise, automatically transferring part of each paycheck into savings removes the need to make the same decision every month. By designing systems that encourage positive behavior, people rely less on motivation and more on consistency.

Lasting financial improvement rarely happens because someone suddenly becomes more disciplined. It happens because they gradually reshape the daily habits that influence hundreds of financial decisions each year.

Financial Freedom Is More About Control Than Luxury

When people imagine financial freedom, they often picture expensive homes, luxury cars, or unlimited spending. While these images are common, they overlook the true value of wealth. Financial freedom is not simply the ability to buy more things; it is the ability to make life decisions without being controlled by money.

A person with financial freedom can leave a job that damages their health without fearing immediate financial collapse. They can take time to learn new skills, start a business, or spend more time with family because they have built a financial cushion. Their money provides flexibility rather than just possessions. This kind of security is often far more valuable than owning luxury items that require constant maintenance and high monthly expenses.

Many people unknowingly sacrifice freedom in exchange for appearance. They purchase homes that stretch their budgets, finance expensive vehicles, or accumulate debt to maintain a lifestyle they believe reflects success. Although these choices may improve their social image, they also reduce their ability to make independent decisions. Every new financial obligation limits future options.

People who understand the psychology of money often place a higher value on flexibility than on status. They recognize that the greatest benefit of wealth is not attracting attention but creating choices. Having the ability to decide where to work, how to spend time, and which opportunities to pursue is one of the most meaningful rewards that money can provide. In the end, true wealth is measured less by what you own and more by the freedom your financial decisions have created.

Why Financial Confidence Is Built, Not Born

Many people assume that those who manage money well are naturally confident. They appear calm during economic uncertainty, make thoughtful financial decisions, and rarely seem overwhelmed by unexpected expenses. From the outside, it looks as though they were simply born with better instincts. In reality, financial confidence is rarely a personality trait. It is usually the result of preparation, experience, and repeated exposure to responsible financial habits.

Confidence grows every time a person successfully handles a financial challenge. Building an emergency fund, paying off debt, following a budget for several months, or staying invested during a market decline all strengthen the belief that future challenges can also be managed. These experiences gradually replace fear with trust in one’s own decision-making. As confidence increases, people become less likely to panic when faced with temporary financial setbacks.

The opposite is also true. Individuals who constantly avoid dealing with money often become more anxious over time. Ignoring bank statements, postponing financial planning, or avoiding conversations about debt may provide temporary relief, but they increase uncertainty in the long run. The less familiar someone becomes with their financial situation, the more intimidating every decision appears.

This is why taking small, consistent actions is so important. Financial confidence is not created by earning a large salary overnight. It is built by proving to yourself, step by step, that you can make responsible decisions and adapt when circumstances change. Like any valuable skill, confidence develops through practice rather than perfection.

The Emotional Price of Easy Money

People naturally appreciate rewards that arrive quickly and with little effort. Winning money, receiving unexpected bonuses, or making large profits in a short period often creates excitement and optimism. However, easy money can sometimes produce unexpected psychological consequences. Because it was earned with minimal effort, it is often treated with less care than money accumulated through years of disciplined work.

Research in behavioral economics suggests that people tend to assign greater value to resources they have worked hard to obtain. This explains why someone may carefully manage the salary they earned over an entire month while spending an unexpected tax refund or gambling winnings much more freely. The emotional connection to the money is different, even though its purchasing power is exactly the same.

Easy money can also create unrealistic expectations. After experiencing one unusually successful investment or business opportunity, some individuals begin believing that similar results should happen regularly. They may take larger risks, ignore basic financial principles, or underestimate the role that luck played in their earlier success. When reality eventually fails to match those expectations, disappointment often leads to poor decision-making.

Financial stability is usually built on predictable habits rather than extraordinary events. While unexpected opportunities should certainly be appreciated, lasting wealth depends on treating every dollar with the same level of responsibility, regardless of how it was earned. Respecting money means recognizing that its long-term value is determined not by where it came from, but by how wisely it is managed.

Why Every Financial Decision Has an Opportunity Cost

Whenever people spend money, they usually focus on what they are receiving in return. They think about the product they are buying, the experience they will enjoy, or the immediate benefit they expect to gain. What often goes unnoticed is the hidden cost of every financial decision: the opportunities that disappear because of that choice.

Economists describe this as opportunity cost, the value of the best alternative that must be given up when making a decision. Although the concept sounds simple, it has profound implications for personal finance. Spending one thousand dollars on the latest smartphone does not only mean losing that amount of money. It also means giving up everything else that money could have accomplished, such as reducing debt, increasing investments, funding education, or strengthening an emergency fund.

Thinking in terms of opportunity cost encourages more intentional financial behavior. Instead of asking, “Can I afford this?” a more useful question becomes, “What am I giving up by choosing this?” This subtle shift changes the way people evaluate purchases. It moves the focus away from immediate affordability and toward long-term value.

Of course, opportunity cost does not mean every purchase should be avoided. Enjoying life and spending on meaningful experiences are important parts of healthy financial planning. The goal is simply to recognize that every financial decision involves a trade-off. People who consistently consider these hidden costs are often better equipped to align their spending with their long-term priorities instead of making choices based solely on short-term emotions.

Wealth Is a Reflection of Daily Choices

Many people spend years searching for a secret formula that will transform their financial future. They read investment predictions, follow successful entrepreneurs, and wait for the perfect opportunity to change everything at once. While these resources can provide valuable knowledge, they sometimes distract from a much simpler truth. Wealth is rarely created by a single dramatic event. More often, it is the natural outcome of thousands of decisions made over many years.

Every financial choice, no matter how small, contributes to a larger pattern. Saving a portion of each paycheck, resisting unnecessary purchases, investing consistently, learning new skills, and avoiding emotional decisions may seem ordinary on any given day. Yet together, these behaviors gradually shape a person’s financial future. Likewise, repeated overspending, excessive borrowing, or constantly postponing financial planning slowly create problems that become increasingly difficult to reverse.

The psychology of money reminds us that financial success is not determined solely by intelligence, income, or luck. It is shaped by habits, patience, emotional awareness, and the ability to remain consistent even when progress appears slow. Understanding these psychological principles allows people to make better decisions not because they can predict the future, but because they can better manage their own behavior.

In the end, money is more than numbers stored in a bank account or displayed on an investment statement. It represents choices, priorities, and the freedom to build a life based on personal values rather than constant financial pressure. Those who learn to master the psychology behind their decisions discover that true wealth is not only measured by what they own, but by the stability, confidence, and opportunities they create for themselves over time.

Tired of reading books without results? This small practical book gives you proven exercises to focus on your goals, boost income opportunities, overcome distractions, and achieve real success

https://maryamaitouamzzi.gumroad.com/l/tugody

From Zero to Success in Just 90 Days – A Priceless Treasure | The Ultimate Guide to Self-Improvement, Building Positive Habits, Breaking Free from Attachment, Increasing Your Income, Achieving Your Goals, and Unlocking Financial Freedom

https://maryamaitouamzzi.gumroad.com/l/vgeofw

My YouTube channel

https://youtube.com/@basoma-u5i?si=oA3uT2IPxMdYvP2K

Frequently Asked Questions (FAQ)

- Is financial success mainly determined by income?

No. Income certainly creates opportunities, but it does not guarantee financial security. Around the world, there are individuals with high salaries who struggle with debt and financial stress because their spending increases as fast as their earnings. At the same time, many people with average incomes gradually build wealth by living below their means, saving consistently, and making thoughtful financial decisions. Income determines how much money enters your life, but your behavior determines how much of it stays and grows.

- Why do intelligent people still make poor financial decisions?

Intelligence helps people solve complex problems, but money is influenced by emotions as much as logic. Fear, overconfidence, stress, social pressure, and the desire for instant gratification can lead even highly educated individuals to make irrational financial choices. Understanding investments is important, but understanding your own behavior is often even more valuable. Financial success depends on emotional discipline just as much as financial knowledge.

- Can financial habits really be changed?

Absolutely. Financial habits are learned through repetition, which means they can also be replaced through repetition. The process is rarely immediate, but consistent small changes eventually become automatic behaviors. Creating a realistic budget, automating savings, tracking expenses, and learning to delay unnecessary purchases are practical examples of habits that gradually reshape a person’s relationship with money.

- What is the biggest psychological mistake people make with money?

One of the most common mistakes is allowing emotions to make financial decisions. People often spend when they feel stressed, invest when everyone else is optimistic, or sell investments during periods of fear. Emotional decisions usually focus on temporary feelings instead of long-term goals. Learning to pause, evaluate the situation objectively, and follow a financial plan reduces the influence of these emotional reactions.

- Is saving money enough to become wealthy?

Saving is an essential first step because it creates financial stability and protects against emergencies. However, saving alone is usually not enough to build long-term wealth. Inflation gradually reduces the purchasing power of money, which is why investing responsibly becomes equally important. The healthiest financial strategy combines disciplined saving, thoughtful investing, and controlled spending.

- Why do people compare themselves financially with others?

Comparison is a natural human tendency, but modern technology has intensified it. Social media constantly exposes people to carefully selected moments of success while hiding debt, financial struggles, and personal sacrifices. As a result, many individuals compare their everyday reality with someone else’s highlights. This often leads to unnecessary spending and dissatisfaction. Lasting financial success comes from pursuing personal goals rather than competing with other people’s lifestyles.

Final Thoughts

Money is often described as a mathematical subject, but in everyday life it is deeply psychological. Every financial decision reflects habits, beliefs, emotions, and experiences that have been developing for years. While knowledge about budgeting, investing, and saving is valuable, these tools become truly effective only when combined with emotional awareness and consistent behavior.

The most successful people financially are not necessarily those who earn the highest incomes or possess the greatest technical knowledge. More often, they are individuals who understand themselves. They recognize when fear is influencing a decision, resist the pressure to compare themselves with others, remain patient during uncertainty, and continue making responsible choices even when immediate rewards are invisible.

Building wealth is not about finding shortcuts or predicting the future perfectly. It is about creating a mindset that supports good decisions day after day, year after year. Small actions, repeated consistently, eventually become powerful results. Financial freedom is rarely achieved through one extraordinary event; it is built through ordinary habits maintained over a lifetime.

If there is one lesson to remember, it is this: your relationship with money will shape your financial future far more than any investment strategy ever could. When you improve the way you think about money, you naturally improve the way you use it. And when your daily choices begin to reflect patience, discipline, and purpose, wealth becomes not just a possibility, but a predictable outcome.

About the Author

Dr. Mariam is a psychologist and researcher with a Ph.D. in Psychology. Her work focuses on understanding how thoughts, emotions, and behavioral patterns influence everyday decision-making, particularly in the areas of personal development, financial behavior, and mental well-being.

Through her writing, Dr. Mariam aims to bridge the gap between psychological science and real-life challenges by transforming complex concepts into practical, easy-to-understand insights. She believes that financial success is not determined solely by income or intelligence but by the habits, beliefs, and emotional patterns that guide everyday decisions.

Her goal is to help readers develop a healthier relationship with money, improve their decision-making skills, and build lasting financial stability through self-awareness, discipline, and evidence-based psychological principles.