What if the financial freedom you’ve been chasing isn’t about earning more money—but making smarter decisions with the money you already have?

Table of Contents

1. Why Financial Success Starts With the Right Mindset 2. What Wealth Really Means in 2026 3. The Biggest Money Mistakes That Keep People Poor 4. Building a Strong Financial Foundation 5. Smart Investing for Beginners 6. The Best Investment Opportunities in 2026 7. How to Diversify Your Portfolio 8. Passive Income Strategies That Actually Work 9. How AI Is Changing Investing 10. Common Investment Mistakes to Avoid 11. Case Study 12. Frequently Asked Questions 13. Final Thoughts

Why Financial Success Starts With the Right Mindset

Money Doesn’t Change Your Life Overnight

What if the biggest obstacle standing between you and financial freedom isn’t your salary, your education, or even the economy—but the way you think about money?

Many people believe that becoming wealthy requires a very high income or finding the perfect investment. In reality, thousands of people with average salaries build impressive wealth over time, while others earning six figures struggle with debt and financial stress.

The difference is rarely intelligence. It is usually behavior.

Every financial decision you make today affects your future. The coffee you buy every morning, the unnecessary subscription you forget to cancel, the money you save each month, and the investments you make all create long-term results. Wealth is not built by one lucky decision. It is built through hundreds of small, smart choices repeated consistently over many years.

One of the biggest financial myths is that investing is only for wealthy people. That idea may have been true decades ago, but technology has completely changed the financial world. Today, almost anyone can start investing with a relatively small amount of money. Online brokers, low-cost index funds, exchange-traded funds, and automated investing platforms have made wealth building more accessible than ever before.

However, access alone is not enough. Successful investing requires patience, discipline, and realistic expectations. Many beginners lose money because they expect to become rich within a few months. They chase trending investments, panic when markets fall, and abandon their plans before long-term growth has time to work.

Financial success looks boring most of the time. It means saving regularly, investing consistently, avoiding emotional decisions, and allowing compound growth to work over many years. These habits rarely create exciting headlines, but they have created millions of financially independent people around the world

What Wealth Really Means in 2026

When people hear the word “wealth,” they often imagine expensive cars, luxury homes, or designer clothes. While those things represent visible success, they rarely tell the full financial story.

Real wealth is the freedom to make choices without constantly worrying about money.

A wealthy person is not necessarily someone with the highest income. Instead, true wealth belongs to someone who owns assets that continue generating value over time while keeping expenses under control.

In 2026, the definition of wealth has expanded beyond traditional investments. Modern investors now have access to diversified portfolios that may include stocks, index funds, bonds, real estate investment trusts (REITs), dividend-paying companies, high-yield savings accounts, and carefully selected alternative investments.

The goal is no longer simply earning more money. The goal is building assets that continue working even when you are not actively working.

Financial freedom begins when your investments start covering a meaningful portion of your living expenses. Every dividend payment, rental income, interest payment, or long-term capital gain reduces your dependence on a monthly paycheck.

This shift changes the way people think about money. Instead of asking, “How much can I earn this month?” successful investors ask, “How many income-producing assets can I build over the next ten years?”

That simple change in perspective often becomes the foundation of lasting wealth.

The Biggest Money Mistakes That Keep People Poor

Many financial mistakes have nothing to do with income. Instead, they are caused by habits that slowly destroy wealth over time.

One common mistake is lifestyle inflation. Every time income increases, spending increases even faster. A salary raise often leads to a larger house, a newer car, more subscriptions, and higher monthly expenses. While income grows, savings remain almost unchanged.

Another mistake is waiting for the “perfect time” to invest.

Some people postpone investing because they believe markets are too expensive. Others wait for interest rates to change or expect another financial crisis before they begin.

The reality is that consistently investing over many years has historically produced better results than trying to predict short-term market movements.

Emotional investing is another major problem.

Fear encourages investors to sell during market declines, while greed encourages buying after prices have already risen significantly. Successful investors understand that markets naturally experience periods of growth and decline. Instead of reacting emotionally, they follow a long-term investment plan based on their financial goals.

Finally, many people underestimate the power of small financial decisions. Saving an extra $100 every month may not seem significant today, but over decades, consistent investing combined with compound growth can create substantial wealth.

Building financial security rarely depends on dramatic changes. It depends on making good decisions repeatedly, even when the results are not immediately visible. Building a Strong Financial Foundation Before You Invest

Many beginners make the mistake of investing before building a strong financial foundation. They open investment accounts, buy popular stocks, or follow advice from social media without first preparing their finances. While investing is important, it works best when it is supported by healthy financial habits.

The first step is understanding exactly where your money goes every month. Many people know how much they earn but have no clear idea how much they actually spend. Small daily expenses, online subscriptions, food delivery services, and impulse purchases slowly reduce the amount available for saving and investing. Creating a monthly budget is not about limiting your lifestyle. It is about making sure your money supports your long-term goals instead of disappearing without purpose.

An emergency fund is equally important. Life is unpredictable, and unexpected expenses such as medical bills, car repairs, or temporary unemployment can force people to sell investments at the worst possible time. Financial experts generally recommend saving enough to cover three to six months of essential living expenses before taking significant investment risks. This emergency reserve provides financial stability and allows investments to remain untouched during difficult periods.

Managing debt should also become a priority. High-interest debt, especially credit card balances, can grow much faster than most investments. Paying off expensive debt often provides a guaranteed financial benefit because it reduces future interest payments. Once high-interest debt is under control, investors have greater flexibility to focus on long-term wealth building instead of constantly paying interest.

Another important habit is automating savings. Instead of saving whatever remains at the end of the month, successful investors often transfer money into savings or investment accounts immediately after receiving their income. This approach removes emotions from the process and builds consistency. Even relatively small monthly contributions can become significant over many years because compound growth rewards patience more than perfection.

—

# Smart Investing for Beginners in 2026

One of the biggest misconceptions about investing is that it requires deep financial knowledge or large amounts of money. Modern investing has become much more accessible than it was a decade ago. Many online investment platforms allow beginners to start with modest amounts while providing educational resources and diversified investment options.

The first lesson every beginner should understand is the difference between investing and speculation. Investing focuses on owning quality assets with long-term growth potential. Speculation often involves chasing short-term price movements without considering the underlying value of the investment. While speculation can sometimes produce quick profits, it also carries significantly higher risks.

For most beginners, diversification remains one of the safest approaches. Rather than placing all available money into one company or one industry, diversification spreads investments across multiple sectors and asset types. This reduces the impact of poor performance from any single investment and creates a more balanced portfolio.

Index funds continue to attract many long-term investors because they provide exposure to hundreds of companies through a single investment. Instead of trying to identify the next winning stock, index funds allow investors to participate in the overall growth of the market while reducing company-specific risk.

Exchange-traded funds (ETFs) have also become increasingly popular. Many ETFs focus on themes such as artificial intelligence, healthcare, renewable energy, cybersecurity, and dividend investing. These funds provide diversification while allowing investors to focus on industries they believe have strong long-term growth potential.

Successful investing also requires realistic expectations. Markets naturally experience periods of volatility. Prices rise, fall, and recover over time. Investors who remain patient during temporary declines often benefit more than those who frequently buy and sell based on emotions or daily news headlines.

# The Best Investment Opportunities in 2026

Every year brings new investment opportunities, but successful investors understand that not every popular trend becomes a profitable long-term investment. Instead of chasing headlines, they focus on industries supported by strong economic and technological trends.

Artificial intelligence continues to attract enormous global investment. Businesses across healthcare, finance, manufacturing, transportation, education, and cybersecurity are integrating AI into daily operations. Companies providing AI software, cloud infrastructure, advanced semiconductors, and data analytics may continue benefiting as adoption expands worldwide.

Cybersecurity remains another important investment theme. As organizations store increasing amounts of sensitive information online, protecting digital infrastructure has become essential. Governments, financial institutions, healthcare providers, and businesses continue increasing cybersecurity spending, creating long-term opportunities for companies operating in this sector.

Renewable energy also continues evolving as governments invest in cleaner energy production and infrastructure. Solar energy, wind power, battery technology, and energy storage solutions remain important areas for long-term investors who believe the global transition toward sustainable energy will continue over the coming decades.

Healthcare innovation represents another promising sector. Advances in biotechnology, medical devices, personalized medicine, and digital healthcare continue transforming patient care while creating investment opportunities for companies developing new treatments and technologies.

While these industries may offer attractive long-term growth, investors should remember that diversification remains more important than predicting which single sector will outperform. Owning a balanced portfolio reduces unnecessary risk while allowing participation in multiple growth trends simultaneously.

# Why Diversification Is One of the Most Powerful Investment Strategies

Diversification is often described as one of the simplest ways to reduce investment risk, yet many beginners underestimate its importance. Instead of placing all available money into one company, one country, or one industry, diversified investors spread their capital across different types of investments.

Imagine two investors. The first invests everything in one technology company because it has recently performed well. The second invests across technology, healthcare, financial services, consumer goods, energy, and international markets. If one sector experiences a temporary decline, the diversified investor may still benefit from growth in other areas.

Diversification does not eliminate risk entirely, but it reduces the likelihood that one poor investment decision will significantly damage an entire portfolio.

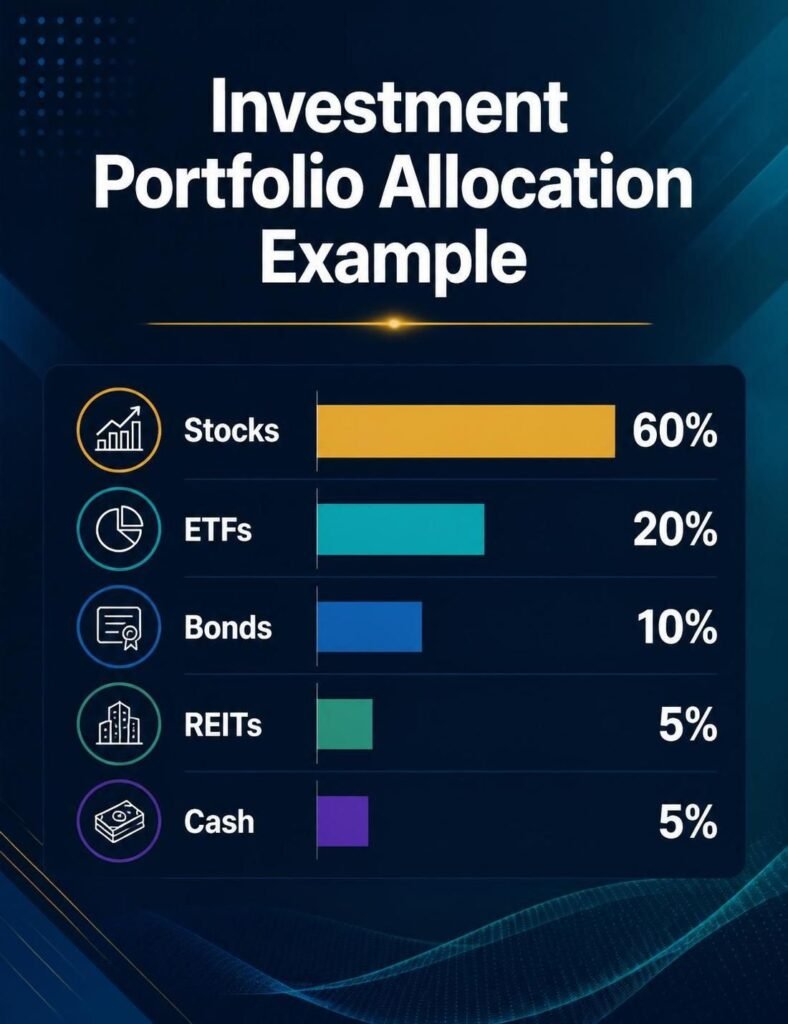

A well-diversified portfolio may include domestic stocks, international stocks, bonds, dividend-paying companies, real estate investment trusts, and cash reserves. The exact allocation depends on an investor’s age, financial goals, and tolerance for risk.

The purpose of diversification is not maximizing returns every single year. Its purpose is creating consistent long-term growth while reducing unnecessary volatility. Investors who remain diversified often find it easier to stay invested during periods of market uncertainty because their portfolios are not dependent on the success of one individual company or one specific industry.

Passive Income: The Secret Behind Long-Term Wealth

One of the biggest differences between financially successful people and everyone else is that they focus on building income that continues even when they are not working.

This is called passive income.

Passive income does not mean earning money without effort. It means doing the work once, building an asset, and allowing that asset to generate income over time.

Some of the most common passive income sources include:

Dividend stocks

Index funds

Rental real estate

REITs (Real Estate Investment Trusts)

High-yield savings accounts

Digital products

Royalties from books or online courses

Instead of depending on a single paycheck, financially independent people usually build multiple income streams.

For example, imagine someone who receives:

$3,000 from a salary

$400 from dividends

$600 from rental income

$300 from digital products

If they lose their job, they still have income coming in. That is why passive income is considered one of the foundations of financial security.

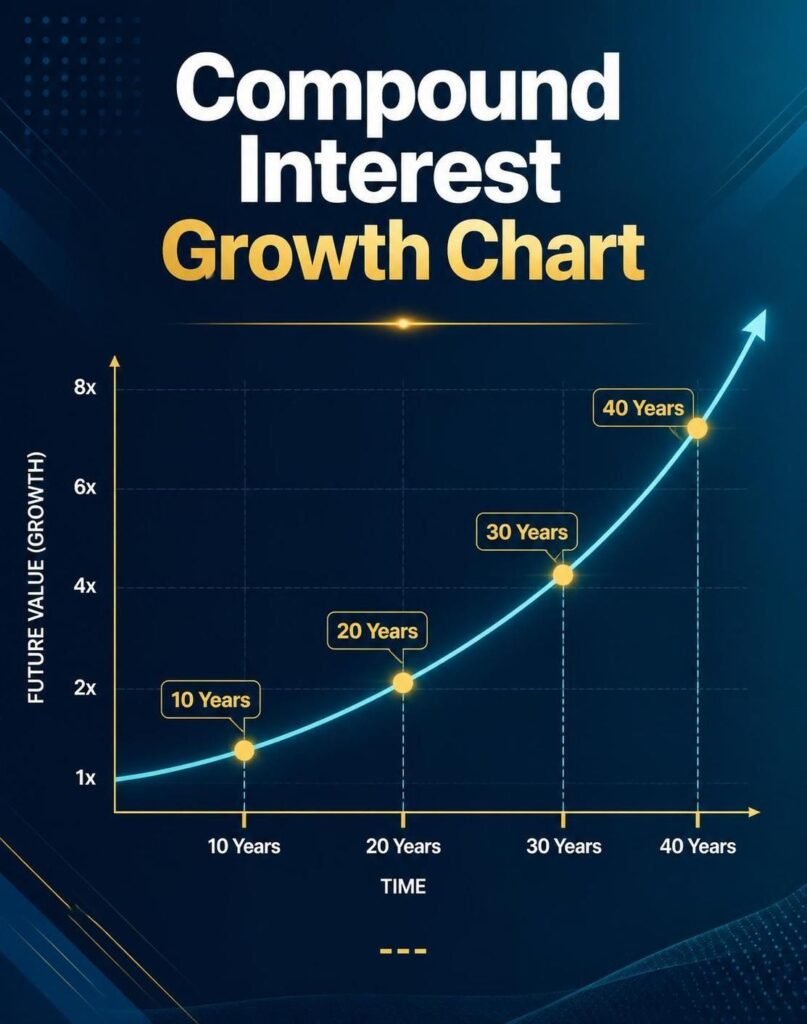

The Power of Compound Interest

Albert Einstein is often credited with calling compound interest “the eighth wonder of the world.” Whether or not he actually said it, the principle itself is one of the most powerful concepts in personal finance.

Compound growth means earning returns not only on your original investment but also on the returns your investment has already generated.

Imagine investing $500 every month for 30 years while earning an average annual return of 10%.

You would invest approximately $180,000 of your own money.

However, thanks to compound growth, the total portfolio could grow to well over $1 million, depending on market performance and fees. This illustrates why starting early can have a dramatic effect on long-term wealth. ([arXiv][1])

The lesson is simple:

The earlier you begin investing, the less money you often need to reach the same financial goal.

Time is usually more valuable than trying to find the “perfect” investment.

What Warren Buffett Can Teach Every Investor

When people think about successful investing, one name almost always appears:

Warren Buffett.

Buffett became one of the wealthiest investors in history not by chasing every market trend but by following a simple strategy for decades.

Since taking control of Berkshire Hathaway in 1965, the company generated an average annual return of about 19.9%, compared with roughly 10.4% for the S&P 500 over the same period. ([Investopedia][2])

More impressive is what happened to investors.

A $100 investment in Berkshire Hathaway in 1965 grew to approximately $5.5 million, while the same amount invested in the S&P 500 grew to around $39,000 with dividends reinvested. ([Morningstar, Inc.][3])

Buffett’s success was not based on predicting tomorrow’s stock prices.

Instead, he followed a few timeless principles:

Invest in businesses you understand.

Think long term.

Ignore market noise.

Never let emotions control your decisions.

Buy quality companies at reasonable prices.

Interestingly, Buffett has repeatedly said that most people do not need to pick individual stocks. For many investors, he recommends low-cost index funds because they provide broad diversification with minimal effort. ([The Motley Fool][4])

His philosophy proves that consistency usually beats excitement.

Ray Dalio: Prepare for Every Market

Another respected investor is Ray Dalio, founder of one of the world’s largest hedge funds.

Dalio believes that nobody can accurately predict every economic event.

Instead of trying to guess what will happen next, investors should build portfolios capable of surviving different economic conditions.

His philosophy emphasizes:

Diversification

Risk management

Emotional discipline

Long-term thinking

Many investors spend their time trying to predict tomorrow’s headlines.

Professional investors often spend more time preparing for uncertainty than predicting it.

That mindset reduces panic during market declines and helps investors stay committed to their long-term plans.

What Statistics Tell Us About Successful Investors

Financial research consistently shows that investor behavior has a greater impact on returns than market timing.

According to DALBAR’s long-running investor behavior studies, many individual investors earn significantly lower returns than the broader market because they buy after prices rise and sell during market declines. Poor emotional decisions—not necessarily poor investments—often explain the gap. ([fa.wellsfargoadvisors.com][5])

Several long-term observations stand out:

Investors who stay invested generally outperform those who frequently trade.

Consistent monthly investing often produces better long-term results than waiting for the “perfect” entry point.

Diversified portfolios typically experience lower volatility than concentrated portfolios.

Time in the market has historically been more important than trying to time the market. ([fa.wellsfargoadvisors.com][5])

These findings reinforce one simple idea:

Successful investing depends more on patience than prediction.

Why Financial Education Is Your Best Investment

Many people spend years learning how to earn money.

Very few spend time learning how to manage it.

Reading one quality finance book every month, following reliable financial news, understanding basic accounting, and learning about investing can improve financial decisions for decades.

Knowledge compounds just like money.

The more you understand investing, taxes, budgeting, inflation, and risk management, the better your financial decisions become.

The wealthiest investors rarely stop learning.

Markets evolve.

Technology changes.

New opportunities appear.

Continuous education allows investors to adapt instead of reacting emotionally.

The goal is not to know everything.

The goal is to know enough to avoid expensive mistakes while making consistently better financial decisions.

https://www.investopedia.com/warren-buffett-s-longevity-in-investing-11727330?utm_source=chatgpt.com “The Secret to Warren Buffett’s Longevity in Investing: 5 Habits To Follow” https://www.fool.com/investing/2025/10/27/warren-buffetts-investing-playbook-simplified-for//?utm_source=chatgpt.com “Warren Buffett’s Investing Playbook — Simplified for First-Time Stock Buyers | The Motley Fool”

How Artificial Intelligence Is Transforming Investing in 2026

Artificial intelligence is no longer a futuristic concept. In 2026, it has become one of the most influential technologies in the financial world. Banks, investment firms, hedge funds, and even individual investors are using AI to analyze data faster, identify market trends, and improve decision-making.

However, there is an important distinction every investor should understand. AI is a powerful tool, but it is not a replacement for financial knowledge or critical thinking.

Many beginners believe AI can predict the stock market with perfect accuracy. The reality is different. Financial markets are influenced by economic events, interest rates, political developments, corporate earnings, and investor psychology. No AI system can accurately predict every market movement.

Instead, successful investors use AI to support their decisions rather than make decisions automatically.

For example, AI can help investors:

Analyze thousands of financial reports within seconds.

Compare company valuations more efficiently.

Monitor investment portfolios.

Identify long-term market trends.

Reduce the time required for research.

The smartest investors combine technology with human judgment.

Inflation: The Silent Wealth Killer

One of the biggest financial risks people often ignore is inflation.

Inflation means that the purchasing power of money decreases over time. Simply put, the same amount of money buys fewer goods and services as prices rise.

Imagine you save $10,000 and keep it in cash for many years without earning interest.

Even though the number in your bank account remains the same, its purchasing power gradually declines if inflation continues rising.

That is why experienced investors rarely keep all of their money in cash.

Instead, they invest in assets that have the potential to grow faster than inflation over the long term.

Historically, diversified stock portfolios have often outperformed inflation over extended periods, although past performance never guarantees future results.

Understanding inflation changes the way people think about money.

Saving is important.

Investing is what helps protect the long-term value of those savings.

Building Multiple Income Streams

One salary can provide financial stability.

Several income streams can provide financial freedom.

One of the most common characteristics of financially successful people is that they rarely depend on only one source of income.

Instead, they build several streams over time.

Examples include:

Full-time employment

Dividend income

Rental properties

Freelancing

Digital products

Affiliate marketing

Online businesses

Investment portfolios

Building multiple income streams does not happen overnight.

Most successful investors begin with one source of income and gradually add another as their financial situation improves.

This approach creates greater financial security because one temporary setback is less likely to affect the entire household.

A Real-Life Example of Long-Term Thinking

One of the most inspiring examples of patience in investing is Warren Buffett.

Although he is known as one of the richest investors in history, a remarkable fact often surprises new investors.

The majority of his wealth was accumulated after the age of 50, and an even larger portion came after the age of 65.

This illustrates an important lesson.

Compound growth becomes increasingly powerful with time.

Many people become discouraged after investing for only two or three years because they do not see dramatic results.

The reality is that wealth often grows slowly at first and much faster during the later years of disciplined investing.

The lesson is simple.

Start early.

Stay consistent.

Allow time to work in your favor.

Case Study: Two Investors, Two Different Futures

Let’s compare two fictional investors.

Investor A

Emma begins investing at age 25.

She invests $400 every month into a diversified portfolio.

She avoids emotional trading and continues investing regardless of market conditions.

When markets decline, she keeps buying because lower prices allow her to purchase more shares.

After many years, her portfolio benefits from compound growth.

Investor B

James waits until age 40 because he believes he needs a higher salary before investing.

He invests larger amounts each month but has fewer years for compound growth.

He also buys and sells frequently whenever financial news creates uncertainty.

Although James invests more money each month, Emma’s longer investment period and disciplined strategy allow her portfolio to grow significantly.

This example demonstrates one of the most valuable investing lessons.

Time often matters more than timing.

Common Investment Mistakes to Avoid

Every investor makes mistakes.

The goal is to avoid the expensive ones.

One common mistake is chasing “hot” investments after they have already experienced massive price increases.

By the time financial news begins promoting a particular investment, much of the initial growth may already have occurred.

Another mistake is checking investment portfolios every hour.

Constant monitoring often increases emotional decision-making.

Many beginners also underestimate investment costs.

Management fees, trading commissions, and taxes may appear small individually, but over decades they can reduce total returns significantly.

Choosing low-cost investment options can improve long-term performance.

Finally, many investors fail because they abandon their plans during market downturns.

Market corrections are normal.

Historically, financial markets have experienced temporary declines followed by periods of recovery.

Patience has rewarded disciplined investors far more often than panic.

Your Financial Future Depends on Today’s Decisions

Financial freedom is rarely created through one extraordinary opportunity.

Instead, it is built through thousands of ordinary decisions repeated consistently.

Every dollar saved.

Every unnecessary expense avoided.

Every investment made.

Every financial book read.

Every lesson learned.

These small decisions gradually create extraordinary results.

The best time to begin building wealth was years ago.

The second-best time is today.

Whether you start with $50 or $5,000, what matters most is developing habits that you can maintain for decades.

Because wealth is not built in a single year

John started investing $200 monthly at age 25. After 20 years with 8% return, his portfolio grew to over $110,000. Frequently Asked Questions (FAQ)

What is the smartest investment for beginners in 2026?

For many beginners, diversified index funds and ETFs remain among the simplest ways to start investing because they spread risk across many companies while requiring very little management.

How much money do I need to start investing?

Many modern investment platforms allow beginners to start with as little as $50 or even less. The most important factor is consistency rather than the initial amount.

Should I invest before paying off debt?

High-interest debt should generally be paid off first. Once expensive debt is under control, long-term investing becomes much more effective.

Is investing risky?

Every investment carries some level of risk. However, diversification, long-term investing, and proper research can significantly reduce unnecessary risk.

What is compound interest?

Compound interest allows your investment returns to generate additional returns over time. This is one of the main reasons long-term investing can produce substantial wealth.

How long should I keep my investments?

Successful investors usually think in years or decades rather than weeks or months. Long-term investing has historically produced more stable results than frequent trading.

What is portfolio diversification?

Diversification means spreading investments across different industries, companies, and asset classes instead of relying on one investment.

Should I invest during a market crash?

Many experienced investors continue investing during market downturns because lower prices may provide better long-term buying opportunities. However, every investor should consider their own financial situation and risk tolerance.

Can artificial intelligence replace financial advisors?

AI can improve research and data analysis, but it cannot completely replace human judgment, financial planning, and personalized investment advice.

How often should I review my portfolio?

Most long-term investors review their portfolios every three to six months instead of checking prices every day.

What percentage of income should I invest?

A common recommendation is investing between 15% and 20% of your income whenever possible, but the right percentage depends on your goals, expenses, and financial responsibilities.

What is the biggest investing mistake?

Allowing emotions to control investment decisions. Panic selling during market declines and chasing popular investments are among the most common mistakes.

Are dividend stocks good for long-term investors?

Dividend-paying companies can provide both regular income and long-term capital appreciation, making them attractive for many investors.

Why is financial education important?

Understanding money management helps people avoid costly mistakes, improve investment decisions, and build long-term financial security.

Can anyone become financially independent?

Financial independence depends on income, savings habits, investment discipline, and time. While every situation is different, consistent financial habits can significantly improve long-term financial outcomes.

Final Thoughts

Building wealth is not about finding the perfect stock, predicting the next market crash, or becoming an expert overnight. It is about making smart financial decisions consistently and giving those decisions enough time to produce meaningful results.

The financial world will continue changing. New technologies will emerge, investment opportunities will evolve, and global markets will experience periods of growth and uncertainty. However, the principles that create long-term wealth remain remarkably consistent.

Spend less than you earn.

Save consistently.

Invest regularly.

Diversify your portfolio.

Think long term.

Keep learning.

Avoid emotional decisions.

These habits may sound simple, but together they create extraordinary financial outcomes.

Remember that every successful investor started exactly where you are today. They didn’t begin with unlimited capital or perfect knowledge. They started by learning, taking action, making mistakes, improving their strategies, and staying committed to their long-term goals.

Your financial future will not be determined by one investment.

It will be determined by thousands of small financial decisions you make over the next five, ten, and twenty years.

Whether your goal is early retirement, financial independence, buying your dream home, creating passive income, or simply achieving peace of mind, the journey begins with one decision.

Start today.

The best investment you will ever make is investing in your financial education.

Ready to start building your wealth?

Explore our investing guides and learn how to make smarter financial decisions every day.

Financial success is not built overnight—but every smart decision you make today brings you one step closer to financial freedom.If you found this guide helpful, explore our other investing and personal finance articles to continue expanding your knowledge. The more you learn, the better your financial decisions become.Start building your future today. Your future self will thank you.

About the Author

Dr. Maryam holds a Ph.D. in Psychology and specializes in behavioral decision-making, personal development, and financial psychology. Through evidence-based articles, she helps readers build smarter financial habits, improve decision-making, and achieve long-term financial success using practical and easy-to-understand strategies.